Intel Takes The Big Restructuring Hits As It Looks Ahead

It is beginning to look like chip maker Intel hit the bottom in its products and foundry businesses in the second quarter of this year and that revenues are slowly – we won’t go so far as to say surely – improving. But now the restructuring charges and cost cutting is going to start to bite and the bottom line will look a little ugly for a while.

Then, Intel will run out of excuses, and hopefully in time for its 18A manufacturing process to catch a little fire among others designing chips for myriad purposes and for 18A processes to be brought to bear on Intel homegrown client and server products. In other words, 2025 should be a hell of a lot better than the misery that 2023 and 2024 was. . . .

We are a long way from the close to 50 percent operating margins that the old Intel Data Center Group used to rake in.

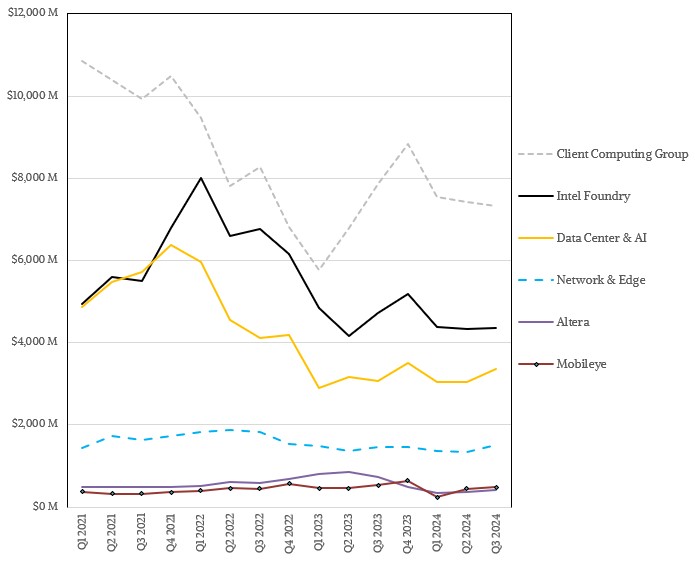

Still, as this chart shows using the new groups that Intel set up in 2022 to describe itself to Wall Street (and that we extended backwards into 2021), things have stopped getting worse, more or less, and that is something. This is the only reason we can think of that Intel’s stock should have gone up in aftermarket trading in the wake of the report to Wall Street. . .

Read more >> Next Platform

.jfif)

.jfif)

.gif)