Orbital data centers have rapidly transitioned from a theoretical concept to a major capital expenditure category. Driven by the explosive compute demands of artificial intelligence and severe terrestrial power constraints, the industry is preparing for initial space-based demonstrator tests as early as next year. [1, 2, 3, 4]

Rather than replacing ground infrastructure, orbital computing will serve as a specialized execution tier optimized for energy-heavy, asynchronous workloads like AI model training and localized space-data processing. [1, 2]

🚀 Who is Driving the Space Compute Race?

A mix of aerospace giants, hyperscalers, and deeply funded startups are filing massive constellation proposals and building hardware: [1, 2]

- SpaceX & xAI: Recently filing an application with the FCC for a gargantuan constellation of up to one million satellites, SpaceX has folded Elon Musk's xAI under its umbrella. Their first-generation hardware, the AI1 satellite, acts as an orbital server rack pushing 150 kW peak power. [1, 2, 3, 4, 5]

- Google: Collaborating with satellite firm Planet, Google's Project Suncatcher aims to launch test satellites equipped with custom, radiation-hardened Tensor Processing Units (TPUs) and 1.6 Tbps optical links. [1, 2, 3]

- Starcloud: Backed by Nvidia, this startup successfully tested an H100 GPU in space and has filed plans for an 88,000-satellite constellation aiming to deliver 20 gigawatts of compute capacity. [1, 2, 3]

- Cowboy Space: Formerly known as Aetherflux, this venture raised $275 million to deploy integrated, one-megawatt satellites capable of both running AI workloads and beaming energy down to Earth. [1, 2]

⚙️ The Critical Engineering Hurdles

The physics of space flip traditional terrestrial data center architecture on its head. The "next phase" of this technology lives or dies by resolving four fundamental engineering challenges: [1, 2]

┌──────────────────────────────────────────────────────────┐

│ Orbital Node Architecture │

├────────────────────────────┬─────────────────────────────┤

│ Power Generation │ Thermal Management │

│ • Continuous solar power │ • Massive liquid radiators │

│ • Dusk/Dawn SSO orbits │ • Heat shed to deep space │

├────────────────────────────┼─────────────────────────────┤

│ Connectivity │ Hardware Longevity │

│ • Terabit-level lasers │ • Radiation hardening │

│ • Starlink mesh routing │ • Micro-satellite swarms │

└────────────────────────────┴─────────────────────────────┘

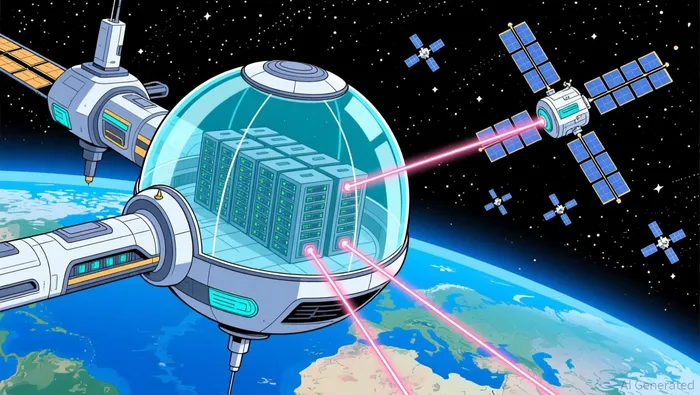

- Thermal Management: Space is a vacuum, meaning data centers cannot use air or water cooling. Because of the square-cube law, giant facilities would melt in orbit. Engineers are forced to build vast swarms of smaller satellites where the exterior hull acts as a radiator. The SpaceX AI1, for example, features a massive 70-meter wingspan consisting mostly of solar arrays and double-sided liquid radiators.

- Power Supply: On Earth, hyperscalers face a broken power grid. Space provides access to unconstrained, 24/7 solar power. Operators plan to utilize Dusk/Dawn Sun-Synchronous Orbits (SSO) to keep the satellites in constant sunlight.

- Laser Interconnects: Moving data back and forth from Earth via traditional radio frequency creates bottlenecks. Next-gen orbital systems rely on free-space optical (laser) links. Individual compute nodes will bridge to one another at terabit speeds and relay the data back to Earth using established networks like Starlink.

- Hardware Depreciation vs. Launch Costs: Terrestrial GPUs depreciate rapidly. In space, hardware cannot easily be swapped out, and launching it remains expensive. The commercial viability of the market—which is projected to reach $39.1 billion by 2035—depends heavily on heavy-lift vehicles like Starship driving launch costs down to the $100–$200/kg range. [1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12]

Hear industry journalists and space technology leaders analyze how terrestrial power constraints are forcing the cloud into orbit:

📅 What Happens Next? (The Timeline)

- 2026–2027 (Demonstrator Phase): SpaceX begins operating its Gigasat factory in Bastrop, Texas, to scale production of AI satellite components. Google, Lumen Orbit, and European initiatives like the ASCEND project deploy early 10-kW to 100-kW federated cluster pilots.

- 2028–2030 (Early Commercialization): Large-scale rack-scale deployments (such as Starcloud 3's 200-kW systems) begin launching via fully reusable heavy rockets.

- 2035+ (The Multi-Gigawatt Era): Thousands of automated micro-satellite swarms form an independent "orbital execution tier" handling massive background AI training cycles, while Earth-based centers specialize in real-time, low-latency applications. [1, 2, 3, 4, 5, 6, 7]

Trending posts and discussions

No comments:

Post a Comment