If you're missing a few details, can't fill-in-the-blanks, or connect-the-dots, there are good reasons why: the deals, zoning changes and title transfers on some over 11,000 acres of city-owned land conveying what are now called "obsolete water-rights" were done over time*

The last bag of money will essentially remove the millions in debt obligations from the city's book by establishing a new escrow account....there's more to the story than that - much more. Readers of this blog might want to go back and watch the uploaded video from last week's study session.

_________________________________________________________________________

Readers of this blog can certainly dig deeper using the Search Box at the top of this blog page or the one in the right-hand margin: Yes, it does take work and time.

Your MesaZona blogger isn't going to make-it-easy for you.

You can type-in: Saints Holding, Natalie Lewis, land barons, Pinal Land Holdings, or New Zion, or Heritage Park.

_________________________________________________________________________

Here's just a take-off point to help you get a grip:

Saints Holding Company

________________________________

This report from Bloomberg helps explain that:

‘It’s Just Dirt’: Anything Goes in Today’s Muni Bond Market

Updated on

". . . The Federal Reserve’s decision to lower benchmark borrowing costs is keeping the U.S. awash in cheap credit. That has fueled a surge in corporate borrowing, bankrolled takeovers of debt-laden companies and, increasingly, sparked concern that some of those leveraged loans have become too risky. That angst has also seeped into the $3.8 trillion market for municipal bonds, a corner of the financial world that traditionally has served as a refuge for individual investors seeking steady, low-risk returns.

With the steep drop in yields wiping out the tax advantages of some tax-exempt securities, investors are hunting for higher payouts. That’s driven yields on the riskiest tax-exempt securities down to about 4%, the lowest since at least 2003, and in turn spurred an increase in sales from the most default-prone segments of the market. Shopping malls, centers for novel health-care treatments, factories seeking to turn trash into fuel and speculative real-estate developments like the one outside of Denver -- all have recently sold tax-exempt debt through local government agencies.

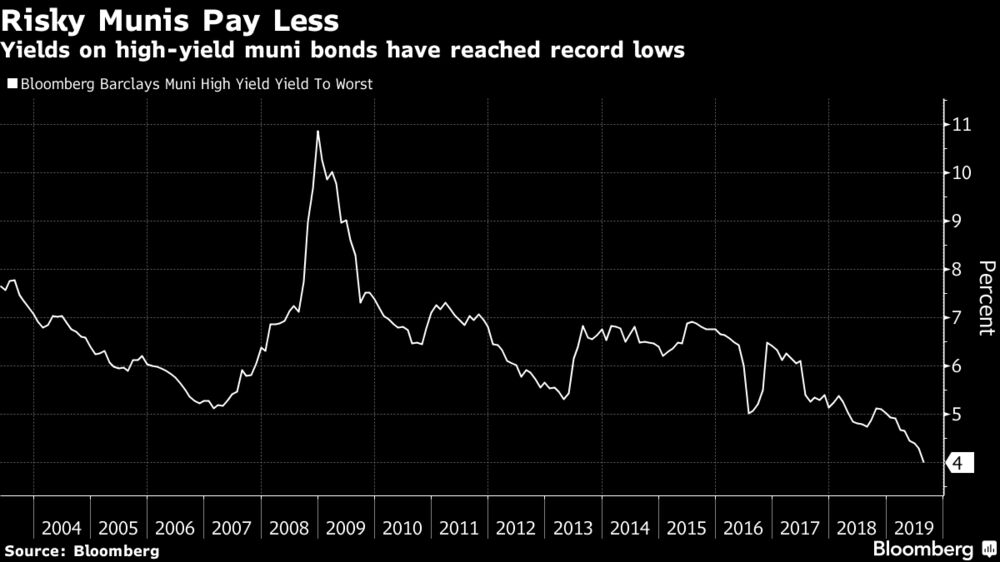

Yields on high-yield muni bonds have reached record lows

The lowest-rated municipal securities have rallied this year, delivering gains of nearly 10%, as plunging yields worldwide leave investors hunting for ways to get higher returns. Mutual funds focused on high-yield tax-exempt debt have pulled in cash every week since early January, with about $384 million added in the week ended Aug. 14, according to Refinitiv’s Lipper US Fund Flows data.

“It is a very aggressive market -- but to say that it is frothy means that this is the end of it, and I don’t know,” said Matt Fabian, a partner with Municipal Market Analytics, an independent research firm. “A year from now, we might be yearning for the discipline of 2019.”