- Destigmatizing the discount window: This is the main way the Fed provides liquidity to banks that need it. Banks force their traders to take vacations to prove that they aren't irreplaceable; similarly, the Fed might force banks to borrow from the discount window to prove that doing so wouldn't cause more harm than good.

- Recalibrating flight risk: Some deposits, including uninsured deposits, are especially prone to bank runs, as we saw at Silicon Valley Bank. Those deposits would register as potentially large outflows to count against the "high-quality liquid assets" that banks need to show.

- Rethinking long-term assets: When a bank intends to hold a loan until it's fully repaid, it doesn't need to account for how much that loan is worth on the secondary market. But if that bank needs cash in a hurry, selling such loans in a fire sale can crystallize losses

- Felix Salmon, author ofAxios Markets

Illustration: Tiffany Herring/Axios

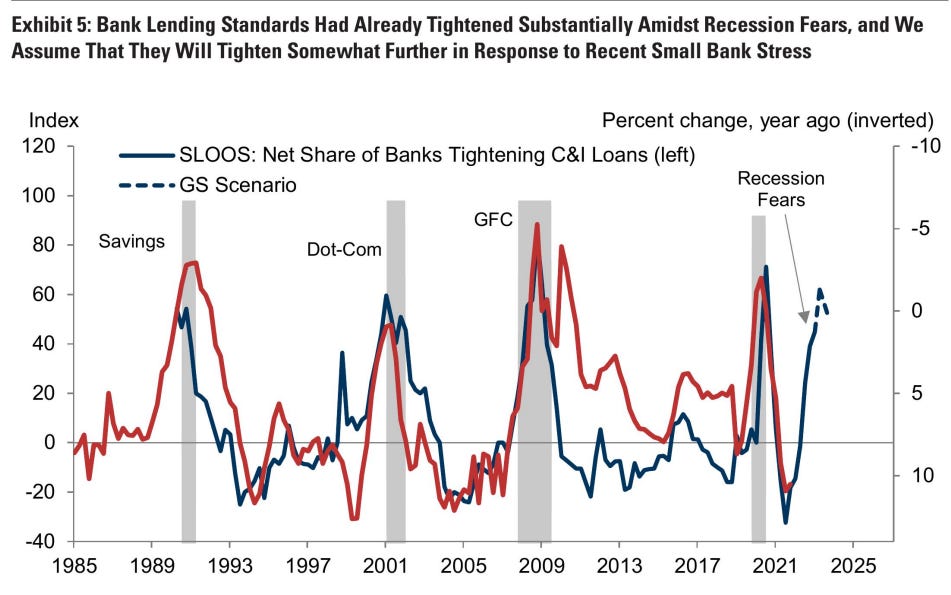

Banks not only need to be strong; they also need to be liquid. That's the message being sent by Federal Reserve officials looking to ensure there won't be a repeat of the banking crisis of one year ago.

Why it matters: Bank regulation moves slowly. Right now regulators are finishing up their response to the financial crisis of 2008 — and are just beginning their response to the 2023 crisis.

What they're saying: "We are working on a package of liquidity measures which directly addresses the Silicon Valley Bank situation," Fed chair Jerome Powell said in congressional testimony Wednesday.

The big picture: The global financial crisis of 2008, and the regulatory response to it, were both centered on institutions deemed "too big to fail."

- Those banks were given a name — global systemically important banks, or G-SIBs — and brought under a much more robust regulatory regime, focused on ensuring they have enough capital to withstand severe economic and financial shocks and still remain solvent.

- The final part of that regulatory push, the highly controversial Basel Endgame, is currently preoccupying much of the financial sector.

Where it stands: The experience of 2023 reminded regulators that there are many large banks, like Silicon Valley Bank, that are small enough to fail but still systemically important.

- It also demonstrated the crucial importance of liquidity, rather than solvency.

A potential run on the bank is probably the biggest and most existential risk that any depository institution faces — and that risk therefore needs to be carefully managed.

Driving the news: Jeanna Smialek and Rob Copeland of the NYT report that the Fed is envisaging a major overhaul of how it regulates bank liquidity. The plan involves three main provisions:

- Destigmatizing the discount window: This is the main way the Fed provides liquidity to banks that need it. Banks force their traders to take vacations to prove that they aren't irreplaceable; similarly, the Fed might force banks to borrow from the discount window to prove that doing so wouldn't cause more harm than good.

- Recalibrating flight risk: Some deposits, including uninsured deposits, are especially prone to bank runs, as we saw at Silicon Valley Bank. Those deposits would register as potentially large outflows to count against the "high-quality liquid assets" that banks need to show.

- Rethinking long-term assets: When a bank intends to hold a loan until it's fully repaid, it doesn't need to account for how much that loan is worth on the secondary market. But if that bank needs cash in a hurry, selling such loans in a fire sale can crystallize losses

- The bottom line: Banks now face two big regulatory overhauls. They probably won't much like either of them.

Go deeper: How "credit risk transfers" could help banks shore up their balance sheets

19 January 2024

Now Required: Emergency Loans Once-A-Year from The Fed's BTFP Facility

US regulators are preparing to introduce a plan to require that banks tap the Federal Reserve 's discount window at least once a year to reduce the stigma and ensure lenders are ready for troubled times.

No comments:

Post a Comment