That settlement did not resolve what kinds of fees Visa and Mastercard could impose, and not all retailers were covered by it.

NEW YORK –

Visa and Mastercard have reached an estimated $30 billion settlement to limit credit and debit card fees for merchants, with some savings likely to be passed on to consumers through lower prices.

The antitrust settlement announced Tuesday is one of the largest in U.S. history, and if it receives court approval would resolve most claims in nationwide litigation that began in 2005.

Some critics believe it may not go far enough, saying the savings would be temporary and that fees would remain high.

Merchants have long accused Visa and Mastercard of charging inflated swipe fees, or interchange fees, when shoppers used credit or debit cards, and barring them through "anti-steering" rules from directing customers toward cheaper means of payment.

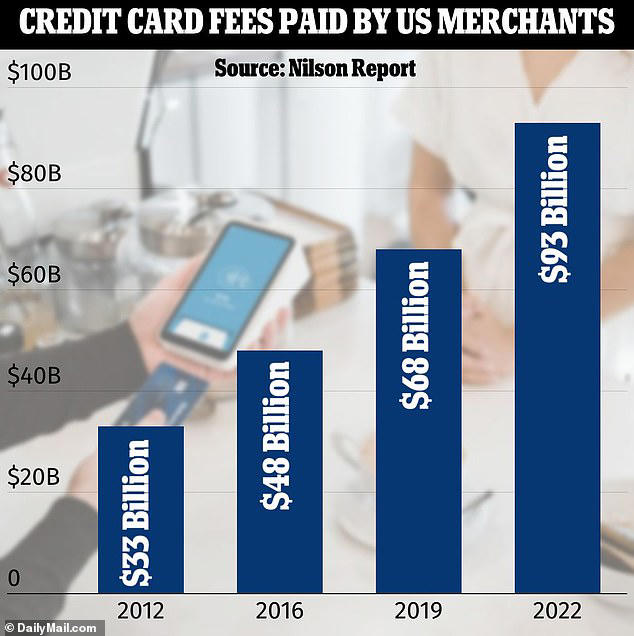

Swipe fees typically include small fixed fees plus a percentage of total sale amounts, and average about 1.5% to 3.5% per transaction according to Bankrate.com.

- Under the settlement, Visa and Mastercard would reduce swipe rates by at least four basis points — 0.04 percentage points — for three years, and ensure an average rate that is seven basis points below the current average for five years.

- Both card networks also agreed to cap rates for five years and remove anti-steering provisions.

Many already warn customers at checkout they will pay more using cards instead of cash.

Opposition expected

Some merchants opted out of that settlement and are pursuing separate lawsuits seeking damages.

Adam Levitin, a Georgetown University professor of law and finance, wrote in an email that those merchants might object to Tuesday's settlement because it would bind them.

- Levitin said U.S. merchants would still pay an average 219 basis point swipe fee, the highest in the developed world.

Tuesday's settlement requires approval by U.S. District Judge Margo Brodie in New York City's Brooklyn borough, likely not before late 2024 or early 2025, and appeals are possible.

"It's a bad deal for merchants," said Doug Kantor, general counsel of the National Association of Convenience Stores, in an interview.

"It provides very small, very temporary relief, but afterward Mastercard and Visa will be free to raise rates, and the agreement doesn't provide a mechanism to slow an increase."

The Retail Industry Leaders Association, which represents businesses that employ more than 42 million Americans, said the settlement required closer review but amounted to "a mere drop in the bucket."

Concessions

- But he said the accord reflects "extraordinary concessions" by Visa, Mastercard and banks because merchants can impose surcharges on airline and cash-back credit cards, though few may because they would rather complete sales than save on fees.

Joseph Stiglitz, a Nobel Prize-winning economist and expert hired by the settling merchants, said in an affidavit that the settlement could provide them with "very substantial" savings.

Darrin Peller, an analyst at Wolfe Research, wrote that Tuesday's settlement "likely takes some wind out of the sails" of that effort. . .

Visa and Mastercard denied wrongdoing in agreeing to settle.

___________________________________________________________________________________

___________________________________________________________________________________

___________________________________________________________________________________

No comments:

Post a Comment