Treasury Rally Risks Running Into a $125 Billion Brick Wall

, Bloomberg News

(Bloomberg) -- Bond traders welcomed their first clear sign of a cooling US labor market, but it’s only a part of what’s needed to fire up the truly sweeping rally they’ve been hoping for all year.

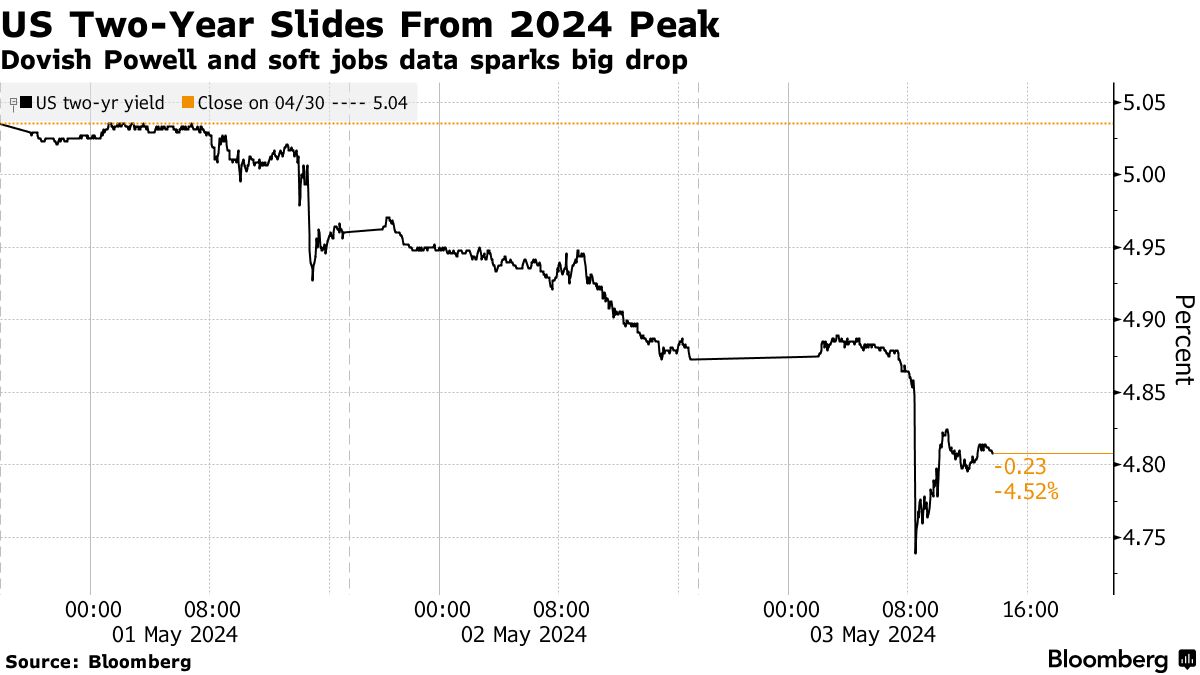

US Treasuries surged Friday after a government report showed surprising softness in jobs and wage gains last month, adding to other recent evidence of slowing growth. The news crowned a late-week advance that started Wednesday after Federal Reserve Chair Jerome Powell pushed back on the need to raise rates and signaled cuts were coming as soon as warranted by the data.

Investors are now cautiously upping their bets for easing this year, and yields on Fed-sensitive two-year notes are leading market gains. And yet, for all the signs of deceleration in some areas of the US economy, inflation remains sticky — a reality that may limit what the central bank can do and means bond yields are likely stuck in their recent ranges.

On top of all that, auctions next week of a combined $67 billion of 10- and 30-year Treasury securities will test demand for longer-dated debt, which has soured among some investors. The government will also sell $58 billion of three-year notes as part of its so-called quarterly refunding auctions.

The jobs report and Powell’s comments were “a relief for the market, but by no means are we pounding the table and thinking we are are going 50 to 100 basis points lower,” said Mark Lindbloom, a portfolio manager at Western Asset Management, which oversees about $385 billion. He sees shorter-term US securities such as two- and five-year notes outpacing longer-term debt.

Powell said policy is restrictive enough to eventually tame inflation and also reminded investors that the Fed would react to signs of weakening job creation and wages. That dovish tilt was underlined in the wake of Friday’s employment data, when at one point the US two-year yield fell to 4.7%, some 30 basis points lower than their high for the year of 5.04% reached on Tuesday. The benchmark was at 4.81% on Friday afternoon.

Curve Calculations

In the month leading up to last week, traders had clawed back wagers for multiple rate cuts this year amid data pointing to relentless growth and persistent inflation. Now, market pricing reflects expectations for almost two full cuts instead of just one as of earlier last week.

While some rate cuts will keep the two-year yield below last week’s peak, the outlook for 10- and 30-year bonds is less compelling for investors should inflation remain above the Fed’s target and Washington’s spendthrift ways result in another rise in long-end auction sizes.

George Catrambone, head of fixed income, DWS Americas prefers owning the two-year “as the probability of rate hikes remains remote,” and remains “skeptical of the outer reaches of the curve,” and has been for “quite some time.”

After flirting with a fresh 2024 peak of 4.75% last week, the 10-year was trading at 4.5% Friday. Any cheapening before the 10-year sale would see the issue provide a 4.5% fixed coupon, equating with the one briefly provided in November, the highest since 2007. While that looks good historically, plenty of investors are wary of fully embracing longer-dated debt right now.

Read more: Bill Gross Says ‘Total Return’ Strategy He Pioneered Is ‘Dead’

“The back end is more vulnerable to repricing higher in yields” than “capped” front-end rates, said Jennifer Karpinski, managing director at Jennison Associates, which oversees $50 billion in fixed income assets.

Jennison favors “a steepening trade strategy” in their portfolios, whereby they are overweight two-, three-, and five-year US Treasuries, while being underweight the 10-year note. “It’s hard to call when the long end does become attractive.”

A steeper curve is in store should the Fed begin cutting and the market prices in more easing on softer data. That would result in the US two-year yield falling faster than longer-dated benchmarks. For would-be buyers of the long end, the real payoff is that inflation will moderate and allow the long end to join a front-end led rally.

What Bloomberg Intelligence Says ...

“The payrolls report for April hints wage growth may be slowing. The Federal Reserve remains data dependent so the Treasury market could stay volatile within defined ranges as data might be mixed near term.”

— Ira F. Jersey and Will Hoffman, BI strategists

Click here to read the full report

The data remains mixed. Countering Friday’s jobs numbers, separate reports last week revealed stubborn pricing pressures in manufacturing and services.

“Three months from now we could be looking at a very different picture on inflation,” said Mark Spindel, chief investment officer at Potomac River Capital, based in Bethesda, Maryland, who has been adding Treasuries across the curve. “I’m back to being more constructive on the outlook for rates, that they can fall.”

Another path toward a steeper curve comes from the back end becoming more sensitive to inflation staying elevated and prompting investors to demand more compensation to own longer-dated Treasuries. This so-called term premium based on the New York Fed model remains slightly negative and some investors think a true normalization from the recent ultra-low rate era equates to a positive reading.

“You’re still not seeing term premium come back into the long end and at some point we do think it comes back,” said Karpinski. “On the refunding, they are not increasing auction sizes for now, but if they do rise over time, it’s another factor that can drive yields up in the long end.”

No comments:

Post a Comment