3h ago

PBOC Signals Possible Government Bond Sales to Cool Market Rally

, Bloomberg News

(Bloomberg) -- The People’s Bank of China said it will borrow government bonds from primary dealers, a sign it may be contemplating selling securities to cool down a market rally.

China’s central bank has decided to borrow bonds from some dealers in order to maintain the steady operation of the bond market, it said in a statement. The decision was made after “careful observation and evaluation” of the current market situation, it said.

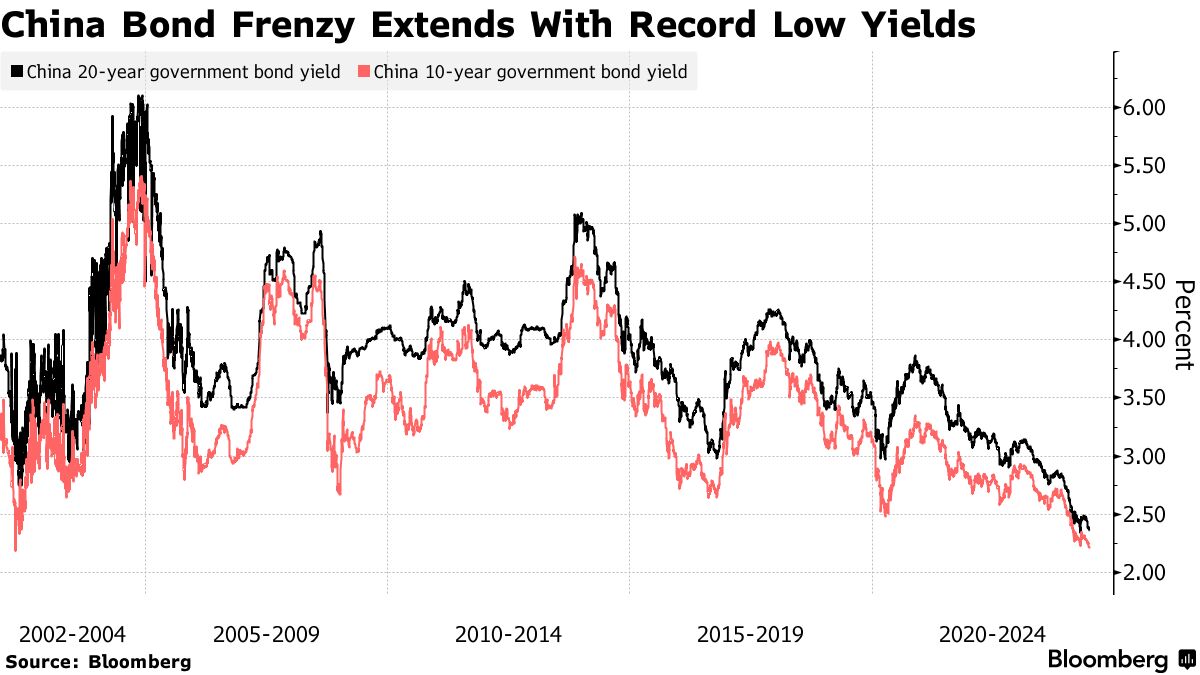

The move came on the heels of a drop in China’s benchmark sovereign yields to a record low earlier Monday, as investors continued to snap up the notes amid pessimism about the domestic economy. The central bank hinted at bond-selling in May.

Bonds retreated after the statement. China’s 10-year yield rose three basis points to 2.24%, reversing an earlier decline to 2.18%.

Ever since an old speech by President Xi Jinping mentioning PBOC bond trading as a potential tool came to the market’s attention two months ago, market watchers have debated how that would work in practice. Strategists said it would depend on the PBOC’s reasons to buy or sell bonds, be it an attempt to cool the overheated rally or a longer-term plan for better liquidity management in the financial system.

Some had speculated that the PBOC would look to borrow securities from primary dealers or big banks and sell them into the market, though there is little precedent for such a move in the global central bank playbook.

“Without further details, one interpretation is that the PBOC is prepared to sell bonds under monetary operations and as such it starts to accumulate some,” said Frances Cheung, a strategist at Oversea-Chinese Banking Corp. in Singapore. “Another possibility is simply a liquidity injection at the time they borrow the bonds. We should not second guess the underlying intention at this stage.”

Why China’s Central Bank Could Become More Like Fed: QuickTake

Bond Rally

China’s bonds have surged on the back of lackluster growth in the economy, expectations for interest-rate cuts and the impact of ample liquidity in the financial system with loan demand so weak. An increase in government borrowing to boost fiscal stimulus has failed to put off bond buyers.

The PBOC has been pushing back against the rally — in May a newspaper backed by the monetary authority warned that leveraged bond-buying not only amplifies volatility but raises the risk of large losses in the event of a market reversal.

At a forum in Shanghai last month, PBOC Governor Pan Gongsheng said the central bank was studying with the Ministry of Finance the implementation of sovereign bond trading.

A practical issue for authorities is that there may not be enough bonds for them to sell, or at least those with the maturities it wants to guide. The central bank held about 1.5 trillion yuan ($207 billion) of government debt on its balance sheet as of April, mostly special sovereign bonds with shorter maturities.

“The central bank’s move meant that it could begin to sell government bonds via open market operations as soon as this week,” said Ming Ming, chief economist at Citic Securities. “At a time when 10-year yields have fallen to historic lows, selling CGBs helps stabilize long-term bond rates and prevents interest rate risk.”

China watchers are preparing for one of the country’s biggest annual policy meetings later this month, the so-called Third Plenum. Chinese leaders at an economic meeting in December said they were contemplating a “new round of fiscal and tax reform,” sparking hopes that details may be unveiled there.

“The relentless bond rally probably tested the PBOC’s tolerance, especially as we head into the all-important Third Plenum,” said Alex Loo, macro strategist at TD Securities. “The PBOC probably wants to avoid any disorderly moves in financial markets as we approach the event.”

Still, any operations by the PBOC may not drive up long-term yields too much, given the weak underlying economic fundamentals, according to Creditsights Inc.

“Muted credit demand in the real economy and persistent disinflation support duration demand,”said senior analyst Zerlina Zeng. “We don’t believe that the central bank wants to engineer a significantly higher long-end CGB yields as this could squeeze higher funding costs” for local governments.

--With assistance from Ran Li and Jing Zhao.

(Updates move, adds further comment)

As bond yields drop, China's central bank could step into secondary market

China's central bank, concerned about a decline in long-term bond yields, will borrow treasury bonds from primary market traders to maintain liquidity in the market.

No comments:

Post a Comment