Fed Stress Test shows the biggest US banks are strong enough to withstand severe recession

All 32 of the nation’s largest banks successfully passed the Federal Reserve's annual stress test, proving they can absorb over $708 billion in hypothetical loan losses while maintaining regulatory capital requirements

No Immediate Changes: The Fed has frozen the Stress Capital Buffer (SCB) requirements until 2027 while they review and update their stress-testing models.

All 32 of the nation’s biggest banks clear the Fed’s annual ‘stress test’

The test, required under the Dodd-Frank Act, assesses whether banks' capital levels would stay robust despite significant projected losses.

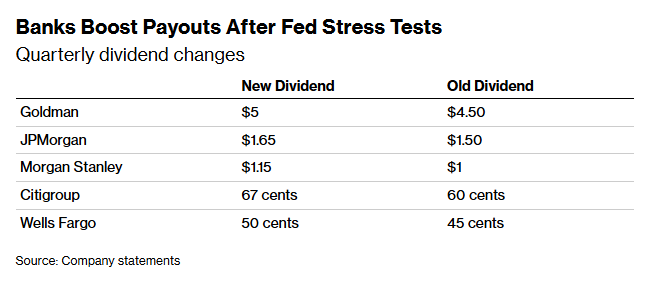

Big banks are paying out record dividends and share buybacks.

getty

In Q1 2026, the eight globally systemically important banks showered shareholders with $46.17 billion in dividends and buybacks — a 34% surge over last year. Twenty years of data reveal a paradoxical pattern: the more uncertain the economy looks, the more aggressively the banks give money away.

$46 Billion in 90 Days

Bank Earnings Releases

In the first three months of 2026 — a period marked by the Iran war, tariff uncertainty, and the most dramatic regulatory shift in bank capital rules since Dodd-Frank — America’s eight largest banks did something that surprised almost no one on Wall Street and almost everyone on Main Street. They handed shareholders $46.17 billion. In ninety days, more than half a billion dollars a day.

To put that in perspective, it is roughly what the United States spends on the entire Environmental Protection Agency over five years. It is, by every measure, a record pace, and it arrived not at a moment of obvious abundance, but at one of unusual economic and market anxiety. This level of payouts and share buybacks is more than about one quarter. It is about a twenty-year shift in how the largest eight globally systemically important banks in the U.S. think about risks and their obligations to shareholders versus responsibilities to ordinary American consumers and the safety and soundness of the banking system.

This shift has made share buybacks the dominant financial instrument of our era, and has elevated a debate among regulators, lawmakers, and economists, that is far from settled.

. . .The Numbers Side by Side: Q1 2025 vs. Q1 2026

SEC Form 8-K earnings releases tell the story of the significant increases in dividend payouts and share buybacks that happened in just one quarter. Every single one of the eight G-SIBs increased both dividends and buybacks year-over-year.

All eight G-SIBs increased both dividends and share buybacks.

Bank Earning Releases

What Q1 2026 Tells Us — And What It Does Not

The Q1 2026 data lands at an unusual moment.

The macroeconomic environment includes geopolitical volatility, elevated recession probability estimates from major forecasters, and tariff-related supply chain uncertainty.

Yet, the banks are returning capital at a record pace.

There are two ways to read this.

1 The optimistic reading: banks are doing this because they genuinely are in good shape — well-capitalized,strong earnings, with fortress balance sheets. JPMorgan posted $14.6 billion in net income in Q1 2026, while Goldman’s trading revenues hit multi-year highs. The buybacks reflect strength, not recklessness.

2 The pessimitic reading,or in my view the realistic one, is what the Minneapolis Fed would offer, that big banks are distributing capital precisely because regulatory pressure has eased, stress test requirements have been relaxed, and no one is stopping them. If — when — the next credit shock arrives, the question of whether these banks have adequate capital buffers to sustain unexpected losses will be answered not by their pre-crisis pronouncements, but by the havoc banks can wreak on Americans who are not on Wall Street.

History, as the twenty-year data makes plain, is unambiguous on one point: the banks that were aggressively buying back stock in 2006 and 2007 were the same banks that needed taxpayer capital in 2008.

The pattern repeats. Whether that represents rational capital allocation, a structural subsidy from the public to shareholders, or simply the natural behavior of institutions operating within the incentives their regulators have constructed — that is the debate that $46 billion in ninety days should force us to have. And I urge bank regulators to have that debate with the banks, which we want to be as safe and as strong as possible for the sake of Americans on Main Street.

Explaining "Rotating Concentration" Out of Mag 7 & Dip in AI Chips

Jun 25, 2026 #micron#earnings#mag7 Liz Ann Sonders with @CharlesSchwab explains what she calls a "rotating concentration" in tech, pointing out that investors are pouring out of the Mag 7 and into other rising tech giants like Micron (MU).

On the "great chip dip" in AI semiconductor names like Nvidia (NVDA), Liz Ann talks about the various factors she sees eating into price action of it and related stocks.

/ schwabnetwork

Follow us on Facebook –

/ schwabnetwork

Follow us on Facebook –  / schwabnetwork

Follow us on LinkedIn -

/ schwabnetwork

Follow us on LinkedIn -  / schwab-network

About Schwab Network - https://schwabnetwork.com/about

#micron #earnings #mag7 #economy #finance #investing #marketnews #stock #stockmarket #trading #live #schwabnetwork #mu #ai #artificialintelligence #chips #software #bigtech #nvidia #nvda

/ schwab-network

About Schwab Network - https://schwabnetwork.com/about

#micron #earnings #mag7 #economy #finance #investing #marketnews #stock #stockmarket #trading #live #schwabnetwork #mu #ai #artificialintelligence #chips #software #bigtech #nvidia #nvda

No comments:

Post a Comment