"For years we've noted how a lack of competition means consumers across the country pay dramatically different prices for the same or worse service. For example a customer in Chattanooga, Tennessee can pay $70 or less for gigabit service, thanks to competition between Comcast and the regionally owned community broadband network.

But live in any of the countless US markets that major broadband providers have neglected (despite decades of major subsidies, tax breaks, and the near-mystical promises surrounding mindless deregulation), and you're often facing the choice of either an apathetic telco with sluggish, neglected DSL, or, more likely, a regional cable monopoly (Charter or Comcast) that charges significantly more money thanks to regional monopolization.

Over at Stop the Cap!, Phil Dampier recently showcased how the presence or absence of competition can even result in customers having to pay up to $40 more per month for the same or sometimes slower service. Not only that, users in more competitive markets enjoy longer promotion rates (often two years rather than just one). Even the fees charged by the regional monopoly (one major way they hit consumers with dramatically higher prices than advertised) are significantly higher at homes that lack any real competition:

"Spectrum charges a hefty $199.99 compulsory installation fee for gigabit service in non-competitive neighborhoods. Where fiber competition exists, sometimes just a street away, that installation fee plummets to just $49.99."

When contacted by Ars, Charter said that "Spectrum Internet retail prices, speeds, and features are consistent in each market—regardless of the competitive environment." But "retail prices" are the standard rates customers pay after promotional rates expire. Stop the Cap showed that Charter's promotional rates vary between competitive and noncompetitive areas.

Charter told Ars that its promotional offers are affected by several factors, including "location."

So while retail (post promotion) rates might be similar from block to block (which often isn't the case regardless of what Charter states), the local cable monopoly uses contract length, promotional rates, and fees to charge significantly different rates. That makes it more difficult for policymakers, consumers, and the press to analyze pricing is quite by design. And it's a major reason why the cable lobby, for years, has fought against the FCC sharing consumer pricing data, knowing full well that once you clearly illustrate the impact of regional monopolization and limited competition, somebody might get the crazy idea to try and actually fix it.

What this "short-form production" from city-owned

and taxpayer-funded Mesa Channel 11 does not tell viewers in the headline subject is the source - an "automated telephone [Robot-call]" survey with 811 responses in a city of more than 525,000.

It was comissioned by the Mesa Police Department, make that paid for, to produce the results they wanted the public to consume.

Telephone surveys have a bad reputation for good reasons.

They are unreliable and easily manipulated.

Furthermore, this is the third attempt in a gang-buster media barrage on June 3, 2021to control the news - this time with hand-held microphones "on-the-street". Believe it if you want to . . .

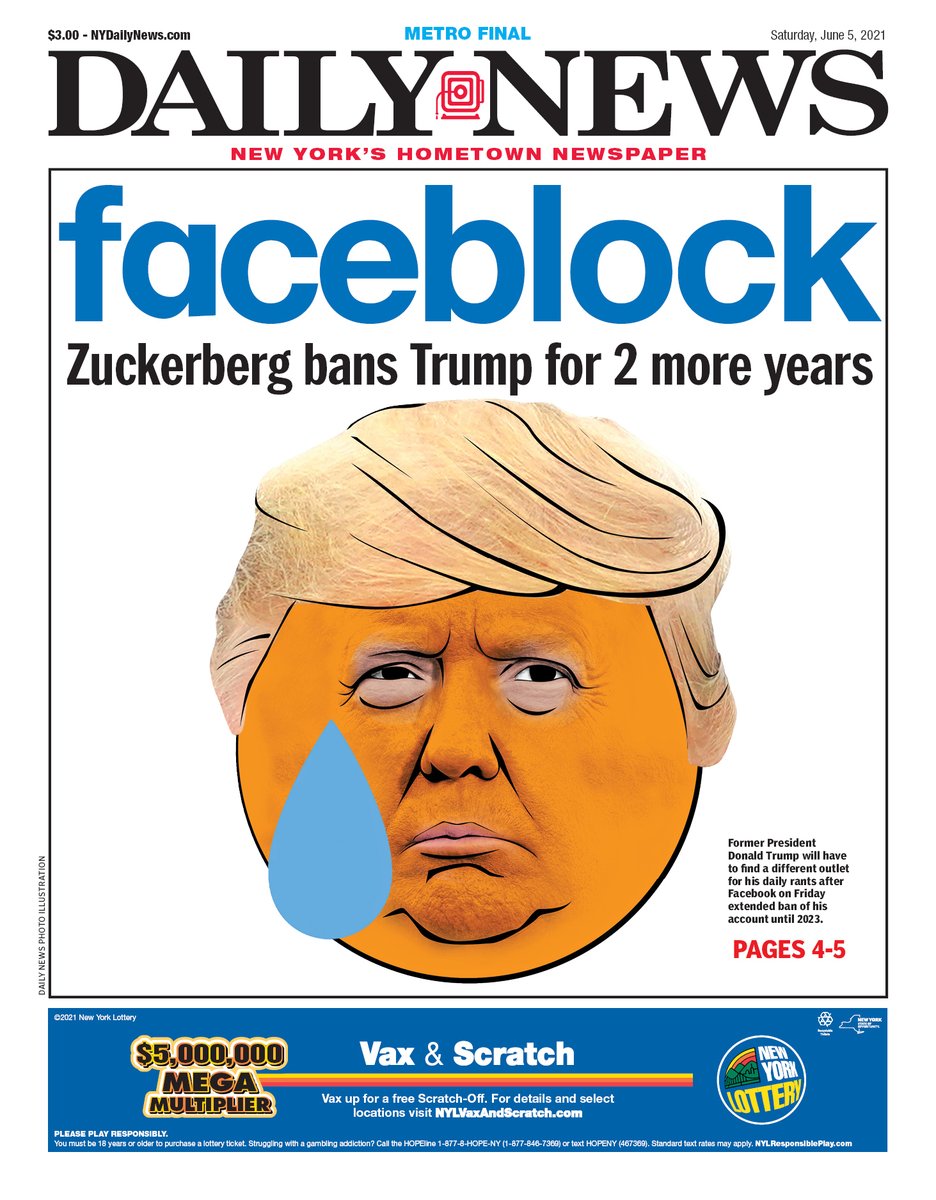

Trump's home-town tabloid hit-the-news-stands with a new emoji plastered on pulp larger-than-life for all the world to see in all its headline glory two days ago on June 5, 2021

(Image taken from social media Twitter)

Looking at top-down line-up from a Google search it's instantly an auction-item on EBay in "unread mint condition" >

Donald Trump Turned Into A Mocking Emoji On New York Daily News Cover

The newspaper reimagined the ex-president after Facebook extended his ban from the platform

". . .Trump was initially booted from Facebook for inciting the deadly U.S. Capitol riot on Jan. 6. On Friday, the company announced the ban would be reassessed on its two-year anniversary, meaning Trump could be back online and free to again post his divisive rhetoric ahead of a possible 2024 presidential run.

“We will evaluate external factors, including instances of violence, restrictions on peaceful assembly and other markers of civil unrest," said Nick Clegg, Facebook’s vice president of global affairs.

“If we determine that there is still a serious risk to public safety, we will extend the restriction for a set period of time and continue to re-evaluate until that risk has receded,” added Clegg, the former deputy prime minister of the United Kingdom.

2 days ago — The newspaper reimagined Trump as the crying-face image on its Saturday cover. “Faceblock,” read its headline, in the social media giant's font.

... talking about this. Breaking news, NYC, national, entertainment, sports and more | 11 Pulitzer Prizes |... ... You were redirected here from the unofficial Page: NY Daily News · Drag to Reposition. Like ... Daily News · 18 hrs ·. FACEBLOCK

It’s Facebook’s house, so we shouldn’t complain too much about what it does—within the law—inside its doors. But there’s something about its new judgment and sentence of Donald Trump, banning him from the site for two years and promising to review his return based on the “risk to public safety,” that screams arbitrary and capricious as opposed to just and consistent. It’s almost as if Facebook deliberately set out to render a verdict in the Trump case that nobody would applaud. It doesn’t overtly offend anybody in the MAGA crowd or the resistance; it appeals to the soft middle that doesn’t really care about Trump, or Facebook, or Facebook’s weaseling jurisprudence.

Nick Clegg, Facebook’s vice president of global affairs and former member of Parliament, took great pride in staking that low ground in his post about the decision. “There are many people who believe it was not appropriate for a private company like Facebook to suspend an outgoing President from its platform, and many others who believe Mr. Trump should have immediately been banned for life,” he wrote. The best you can say for Clegg and the company’s decision is that it was Solomonic but only in the sense that Facebook followed through on its threat to slice the baby in half by doing just that—and doing it as a Friday news dump.

In slamming Facebook for inconsistency, we must also take care to also point out that the social media company is consistent about its inconsistencies.

> Thanks to founder and CEO Mark Zuckerberg’s governance, it practiced inconsistent enforcement of its “hate speech” guidelines and then apologized for those inconsistencies.

> It banned political ads after the November election, then reinstated them in March.

> It banned posts that contradicted Centers for Disease Control and Prevention directions and then lifted the ban.

> Don’t take my word for it: The co-chairman of Facebook’s so-called Oversight Board, appointed to review and judge Facebook’s content policy and actions, called its content-banning policies a “shambles” last month.

“Their rules are a shambles,” Michael McConnell said. “They are not transparent. They are unclear. They are internally inconsistent.”

Facebook thought it had purchased a pass from criticism when it established the Oversight Board in 2020. All the tough questions about running the site could be punted by Zuckerberg to the oversighters, leaving him little to do but trap and spend its $86 billion in annual revenues. . .

Their rules, apparently, are “kick the can two years further down the road.” A normal company and a normal CEO would be ashamed to run its affairs in such a slipshod fashion. But Facebook and Zuckerberg are not normal. He’s the guy who habitually screws up but always apologizes dramatically when found out.

> Fast Company and other outlets have collected and cataloged his apology storms over the years.

> The privacy-invading “Beacon” feature. Zuck was sorry about that.

> Sharing unique user IDs with advertisers? So sorry.

> Calling Facebook users “dumb fucks”?

> Rejecting the argument that Facebook helped Trump win?

> The Cambridge Analytica scandal?

Sorry, sorry, sorry.

There should be a law of limitations that rations public apologies and puts those who exceed the limit into a penalty box for six months.

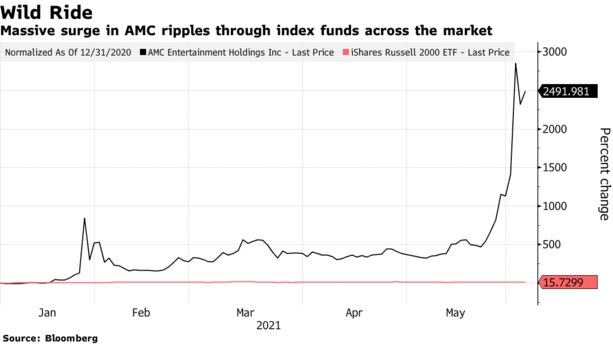

Wild moves in meme shares are roiling the ETF market

Scale of swings, fund plumbing lead to unintended exposures

More Index funds are supposed to cut out the human-driven craziness that periodically infects markets, but the recent meme-stock fever proved the $11 trillion industry is far from immune.

The remarkable surge in shares of AMC Entertainment Holdings Inc. and a handful of other stocks is showing up in multiple exchange-traded funds, skewing portfolios, altering risk profiles and exerting outsized influence on prices. lash markets out of nowhere.

“For index investing, the appeal is that human decision-making, human emotions are taken out of it,” said Tom Essaye, a former Merrill Lynch trader who founded “the Sevens Report” newsletter. . .

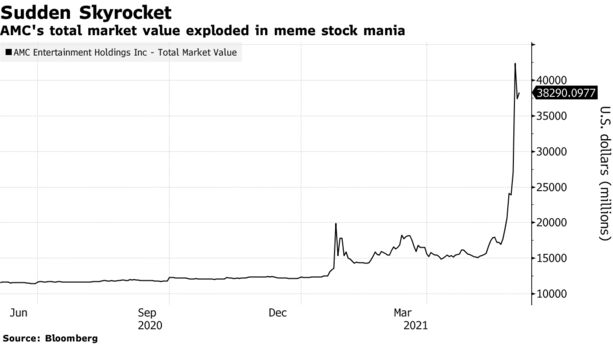

AMC shares currently stand at almost 10 times the level analysts see it trading a year from now: $5.25. The premium tops all Russell 3000 stocks that have enough of an analyst following to generate a price target, according to Bloomberg data, and more than double that of GameStop -- the next over-valued stock.

AMC will likely remain in many value funds until their rebalancing comes around.

“Research tells premiums such as those associated with small cap and value stocks are generally delivered by a subset of the asset class,” said Wes Crill at Dimensional Fund Advisors, a pioneer of quant investing which has $637 billion under management. “Style drift can reduce the odds of capturing the premiums when they appear.”

The obvious solution would be to rebalance more often. But that would bring more transactional costs to funds, which can be a big problem for passive vehicles charging rock-bottom fees.

2

screentime

AMC Stock Sale Comes With Warning to Traders: Be Prepared to Lose It All

Company said entire investment may be lost in offering

It’s uncommon to see such a dire warning in stock sale

More

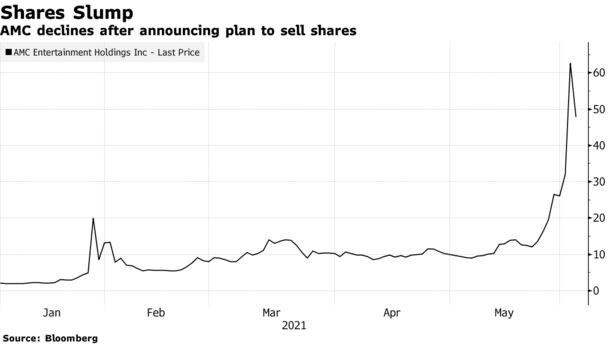

Investing in AMC Entertainment Holdings Inc. comes with the promise of free popcorn, special screenings -- and the chance you’ll lose all your money.

That last part is a warning the movie chain and its lawyers made in a regulatory filing on Thursday announcing its intention to sell more than 11 million shares to a market dominated by frenzied retail traders.

While companies commonly use cautionary language when making share offerings, the extent of AMC’s was uncommon. It included an acknowledgment that the stock is at the mercy of the retail mania, with fundamentals playing little role in determining valuation.

“We believe that the recent volatility and our current market prices reflect market and trading dynamics unrelated to our underlying business, or macro or industry fundamentals, and we do not know how long these dynamics will last,” AMC said in its filing Thursday. “Under the circumstances, we caution you against investing in our Class A common stock, unless you are prepared to incur the risk of losing all or a substantial portion of your investment.”

The movie-theater chain revealed that it plans to capitalize on the rally by selling up to 11.55 million shares to trim its debt load and finance future acquisitions. The tone in Thursday’s filing is starkly different than the one in its announcement a day earlier, when it said it would offer retail shareholders special perks as a reward for their loyalty.

Shares of AMC plunged more than 30% as trading kicked off on Thursday, triggering a halt. They’re are still up more than 2,000% since the beginning of the year. This would be the company’s fourth stock sale of 2021. It sold shares this week to Mudrick Capital, which flipped them on the same day for a profit.

“When a company files to sell more than 11 million shares of stock, you wouldn’t expect to see the above statement connected to the offering,” Paul Hickey, co-founder of Bespoke Investment Group, wrote in a note.

At its recent share price of around $60, AMC could raise $693 million as part of its offering, Hickey said. For perspective, AMC’s total market value at the start of 2021 was around $434 million.

Flash News: Ukraine Intercepts Russian Kh-59 Cruise Missile Using US VAMPIRE Air Defense System Mounted on Boat. Ukrainian forces have made ...

Flash News: Ukraine Intercepts Russian Kh-59 Cruise Missile Using US VAMPIRE Air Defense System Mounted on Boat. Ukrainian forces have made ...