February 10, 2021

Getting Back to a Strong Labor Market

Chair Jerome H. Powell

At the Economic Club of New York (via webcast)

Today I will discuss the state of our labor market, from the recent past to the present and then over the longer term. A strong labor market that is sustained for an extended period can deliver substantial economic and social benefits, including higher employment and income levels, improved and expanded job opportunities, narrower economic disparities, and healing of the entrenched damage inflicted by past recessions on individuals' economic and personal well-being. At present, we are a long way from such a labor market. Fully realizing the benefits of a strong labor market will take continued support from both near-term policy and longer-run investments so that all those seeking jobs have the skills and opportunities that will enable them to contribute to, and share in, the benefits of prosperity.

The Labor Market of a Year Ago

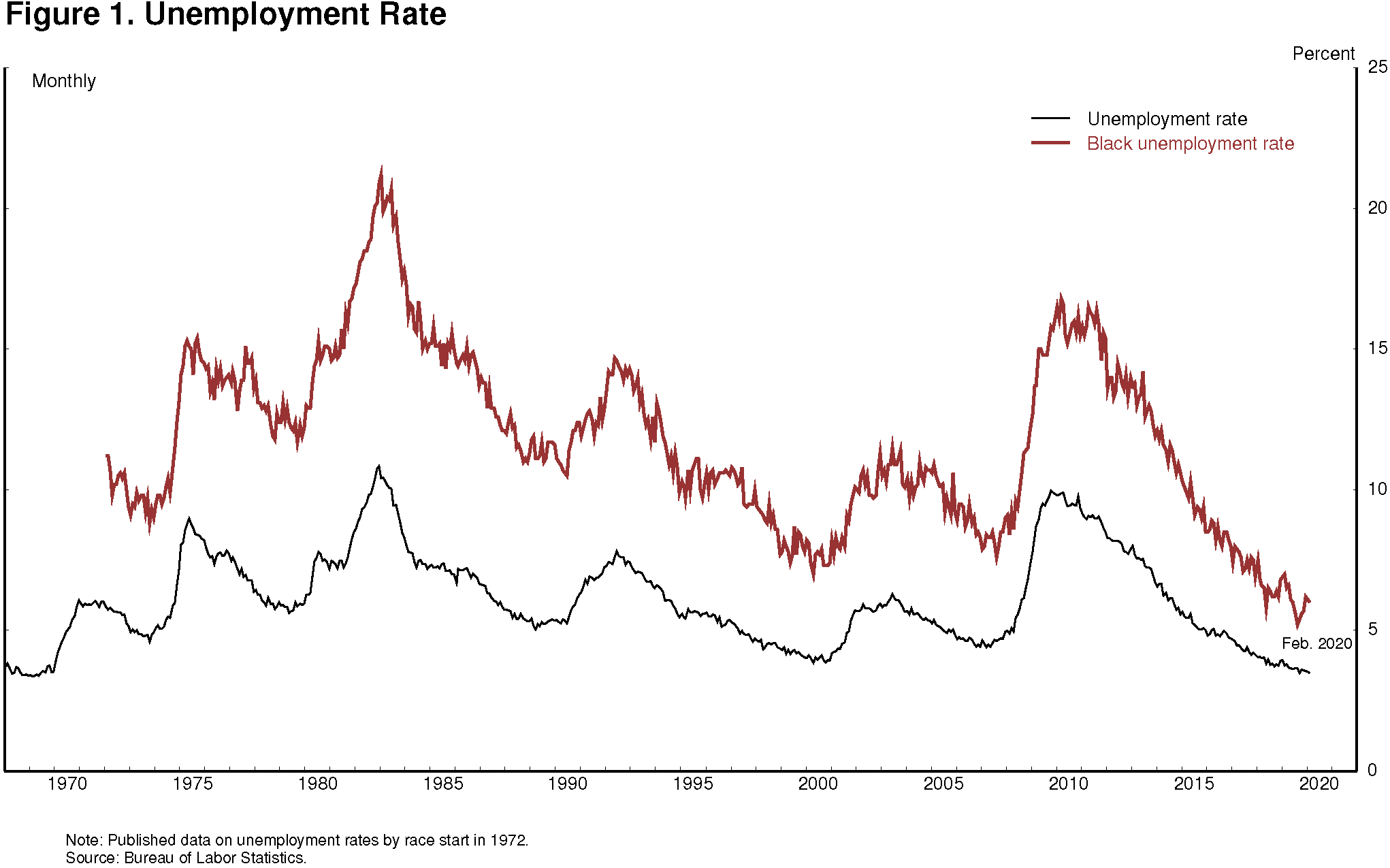

We need only look to February of last year to see how beneficial a strong labor market can be. The overall unemployment rate was 3.5 percent, the lowest level in a half-century. The unemployment rate for African Americans had also reached historical lows (figure 1). Prime-age labor force participation was the highest in over a decade, and a high proportion of households saw jobs as "plentiful."1 Overall wage growth was moderate, but wages were rising more rapidly for earners on the lower end of the scale. These encouraging statistics were reaffirmed and given voice by those we met and conferred with, including the community, labor, and business leaders; retirees; students; and others we met with during the 14 Fed Listens events we conducted in 2019.2

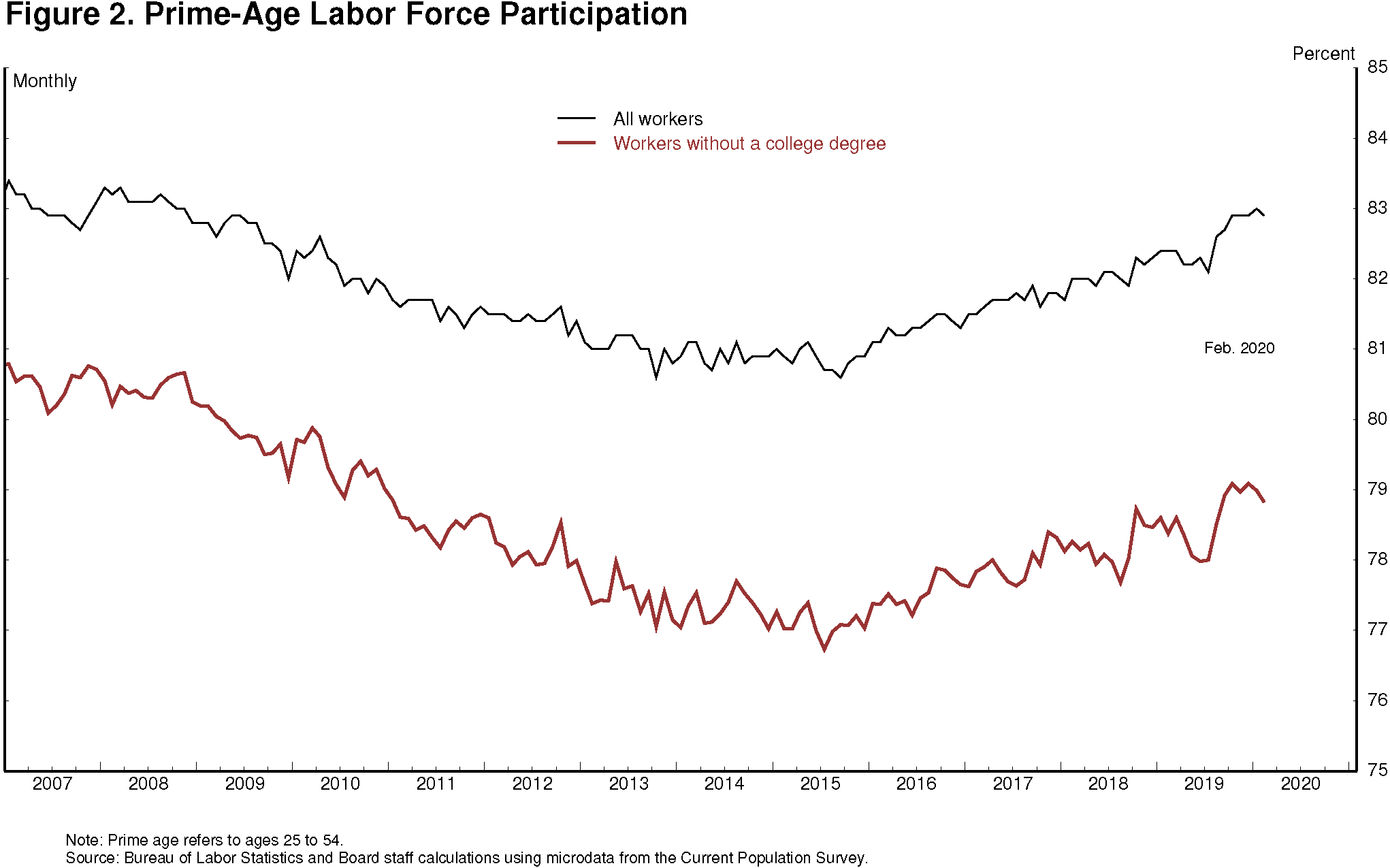

Many of these gains had emerged only in the later years of the expansion. The labor force participation rate, for example, had been steadily declining from 2008 to 2015 even as the recovery from the Global Financial Crisis unfolded. In fact, in 2015, prime-age labor force participation—which I focus on because it is not significantly affected by the aging of the population—reached its lowest level in 30 years even as the unemployment rate declined to a relatively low 5 percent. Also concerning was that much of the decline in participation up to that point had been concentrated in the population without a college degree (figure 2). At the time, many forecasters worried that globalization and technological change might have permanently reduced job opportunities for these individuals, and that, as a result, there might be limited scope for participation to recover.

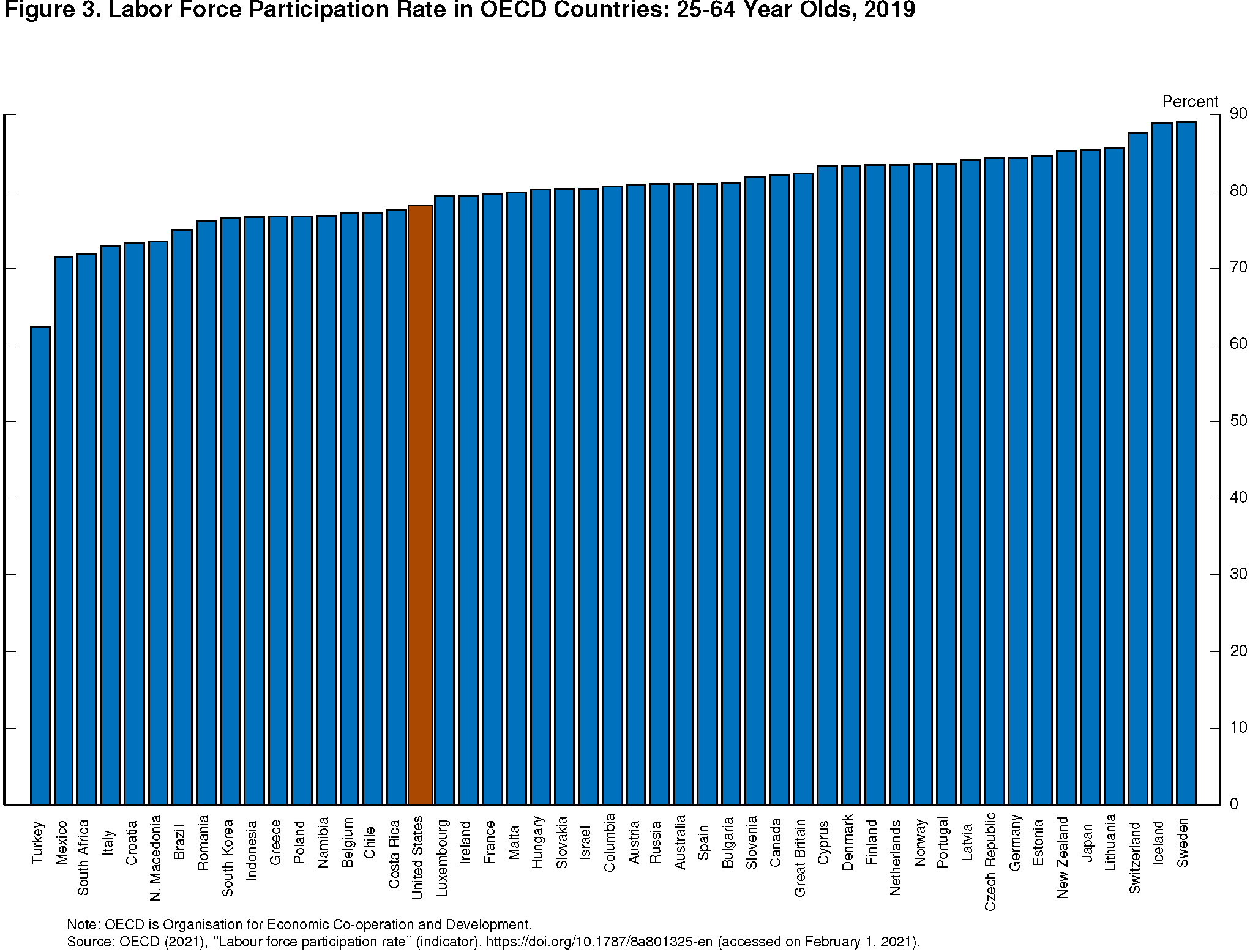

Fortunately, the participation rate after 2015 consistently outperformed expectations, and by the beginning of 2020, the prime-age participation rate had fully reversed its decline from the 2008-to-2015 period. Moreover, gains in participation were concentrated among people without a college degree. Given that U.S. labor force participation has lagged relative to other advanced economy nations, this progress was especially welcome (figure 3).3. . .

The Labor Market Today

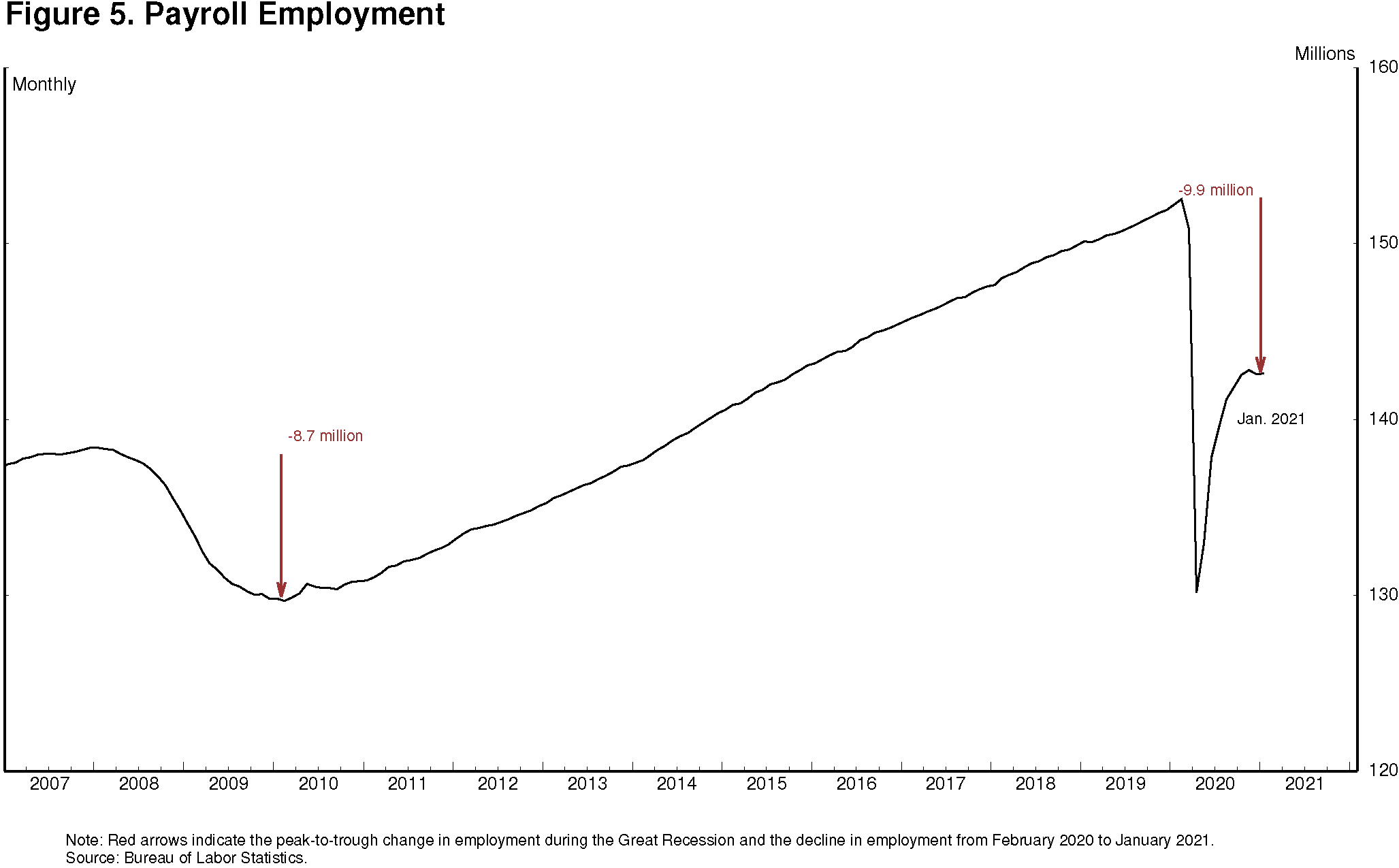

The state of our labor market today could hardly be more different. Despite the surprising speed of recovery early on, we are still very far from a strong labor market whose benefits are broadly shared. Employment in January of this year was nearly 10 million below its February 2020 level, a greater shortfall than the worst of the Great Recession's aftermath (figure 5).

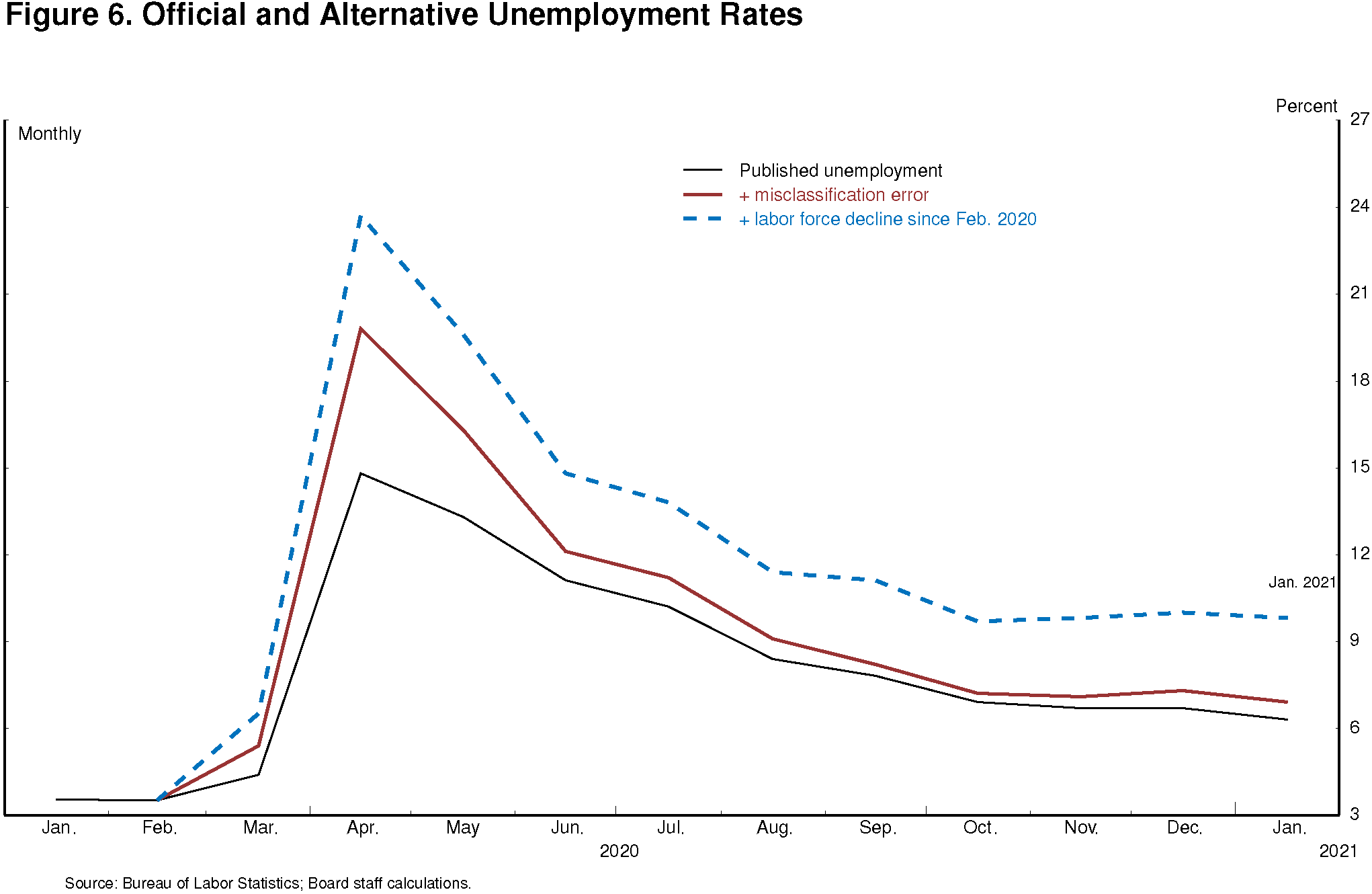

After rising to 14.8 percent in April of last year, the published unemployment rate has fallen relatively swiftly, reaching 6.3 percent in January. But published unemployment rates during COVID have dramatically understated the deterioration in the labor market. Most importantly, the pandemic has led to the largest 12-month decline in labor force participation since at least 1948.5 Fear of the virus and the disappearance of employment opportunities in the sectors most affected by it, such as restaurants, hotels, and entertainment venues, have led many to withdraw from the workforce. At the same time, virtual schooling has forced many parents to leave the work force to provide all-day care for their children. All told, nearly 5 million people say the pandemic prevented them from looking for work in January. In addition, the Bureau of Labor Statistics reports that many unemployed individuals have been misclassified as employed. Correcting this misclassification and counting those who have left the labor force since last February as unemployed would boost the unemployment rate to close to 10 percent in January (figure 6).

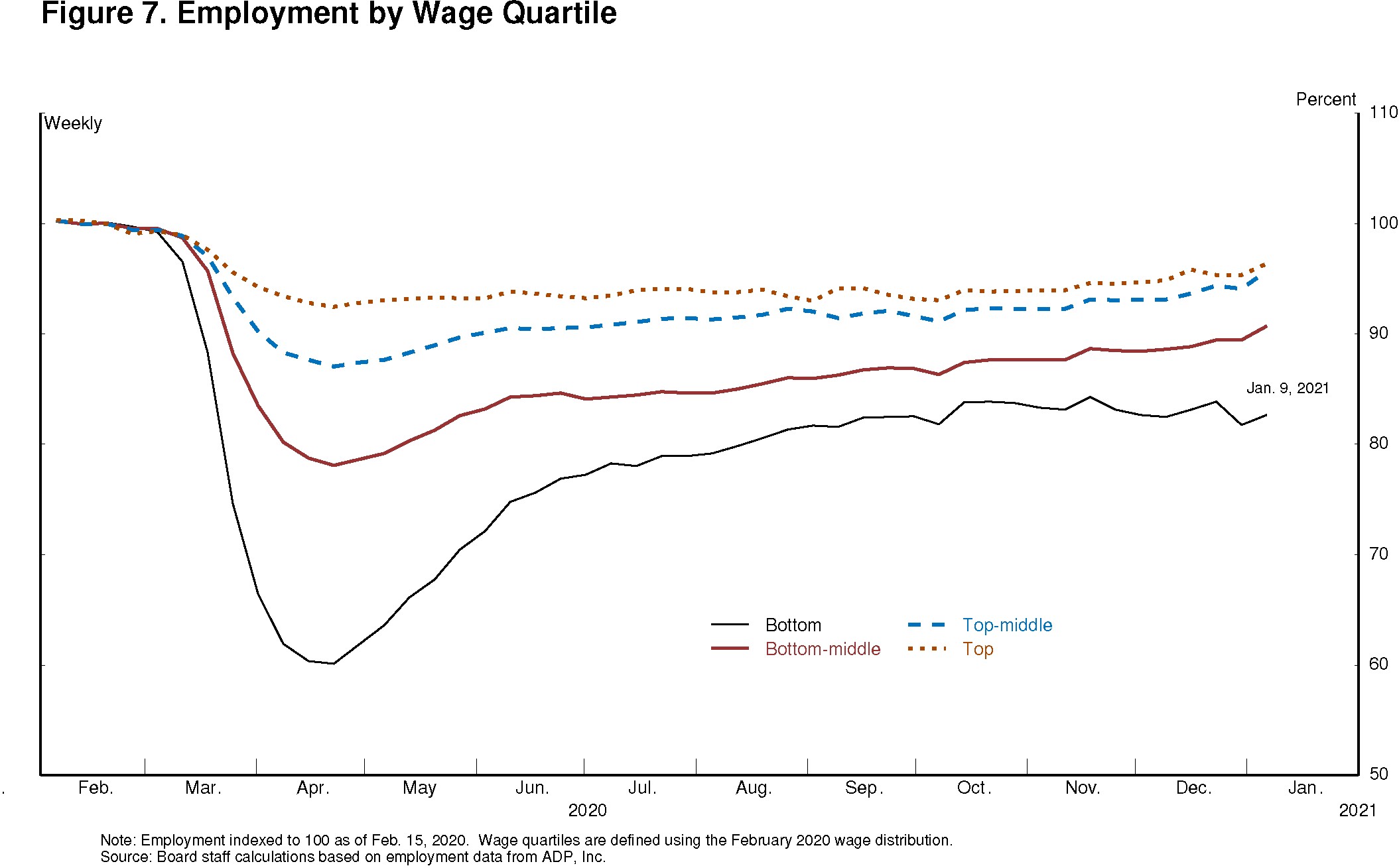

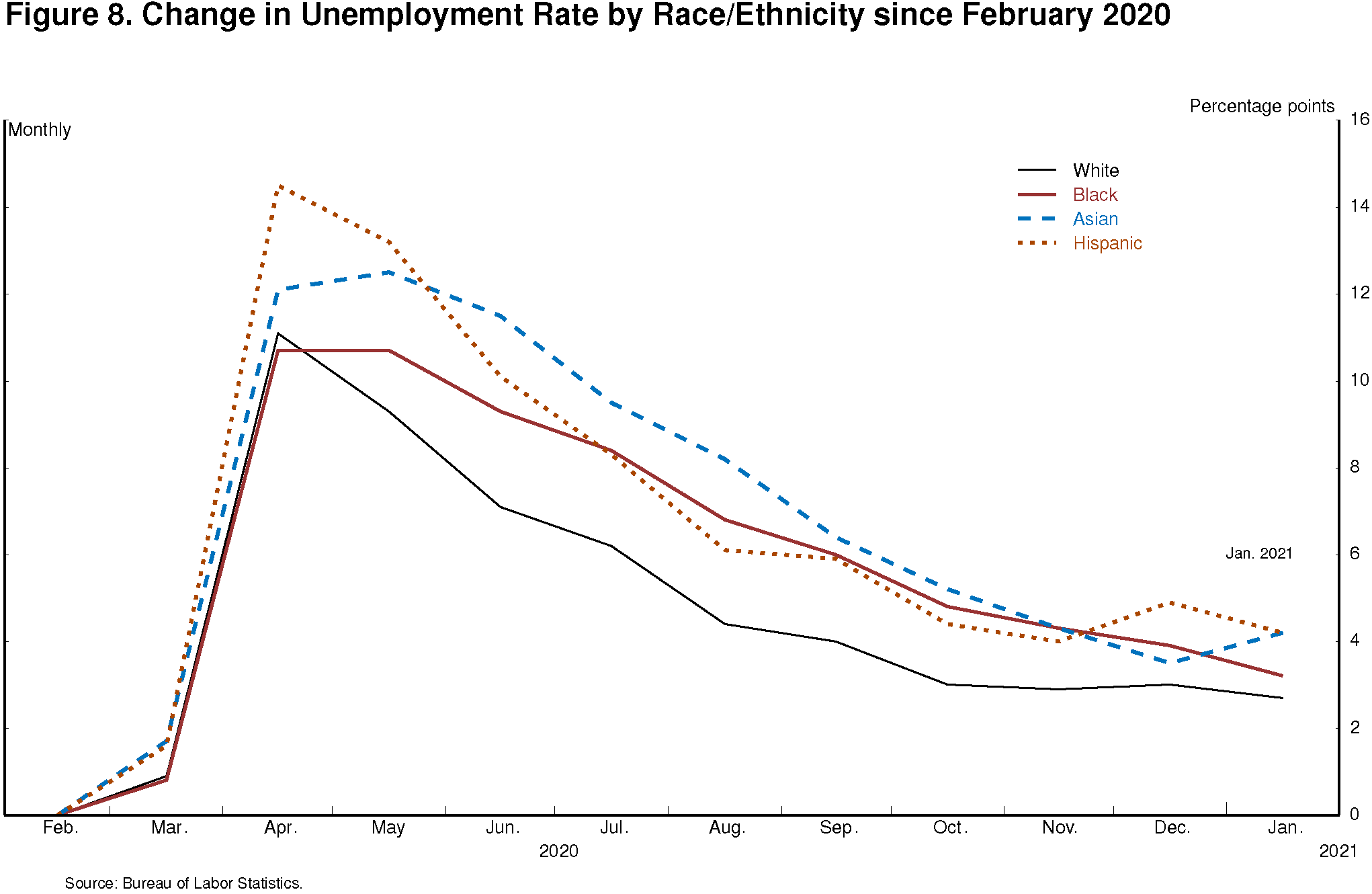

Unfortunately, even those grim statistics understate the decline in labor market conditions for the most economically vulnerable Americans. Aggregate employment has declined 6.5 percent since last February, but the decline in employment for workers in the top quartile of the wage distribution has been only 4 percent, while the decline for the bottom quartile has been a staggering 17 percent (figure 7). Moreover, employment for these workers has changed little in recent months, while employment for the higher-wage groups has continued to improve. Similarly, the unemployment rates for Blacks and Hispanics have risen significantly more than for whites since February 2020 (figure 8). As a result, economic disparities that were already too wide have widened further.

In the past few months, improvement in labor market conditions stalled as the rate of infections sharply increased. In particular, jobs in the leisure and hospitality sector dropped over 1/2 million in December and a further 61,000 in January. The recovery continues to depend on controlling the spread of the virus, which will require mass vaccinations in addition to continued vigilance in social distancing and mask wearing in the meantime.

Since the onset of the pandemic, we have been concerned about its longer-term effects on the labor market. Extended periods of unemployment can inflict persistent damage on lives and livelihoods while also eroding the productive capacity of the economy.6

And we know from the previous expansion that it can take many years to reverse the damage. . .

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

No comments:

Post a Comment