The Trump administration's aggressive tariff policies, spanning 2017 to

2021 and extending into 2025, have reshaped global trade dynamics,

creating a fragmented and volatile economic landscape.

These measures,

framed as a defense of domestic industries, have instead triggered

retaliatory actions,

disrupted supply chains, and

introduced systemic

risks to equity markets

The Global Impact of Trump's Tariff Surge on Equity Markets and Growth Outlook

Isaac LaneFriday, Aug 1, 2025 4:45 am ET

- Trump's 2017-2025 tariffs reshaped global trade, triggering retaliation and equity market volatility.

- U.S. average tariffs hit 22.5%, raising costs for automakers and destabilizing metal markets with 50% copper/aluminum tariffs.

- J.P. Morgan estimates 1% global GDP loss in 2025, with emerging markets facing sharper contractions.

- Equity markets show caution; defensive sectors outperform as tariffs disrupt supply chains and consumer spending.

- Latin America and AI sectors offer asymmetric opportunities amid trade realignments and AI-driven demand.

. As investors navigate this new era, understanding the long-term implications of these policies is critical to identifying both risks and opportunities in a world where trade barriers are no longer temporary but structural.

The Tariff Surge: A Catalyst for Fragmentation

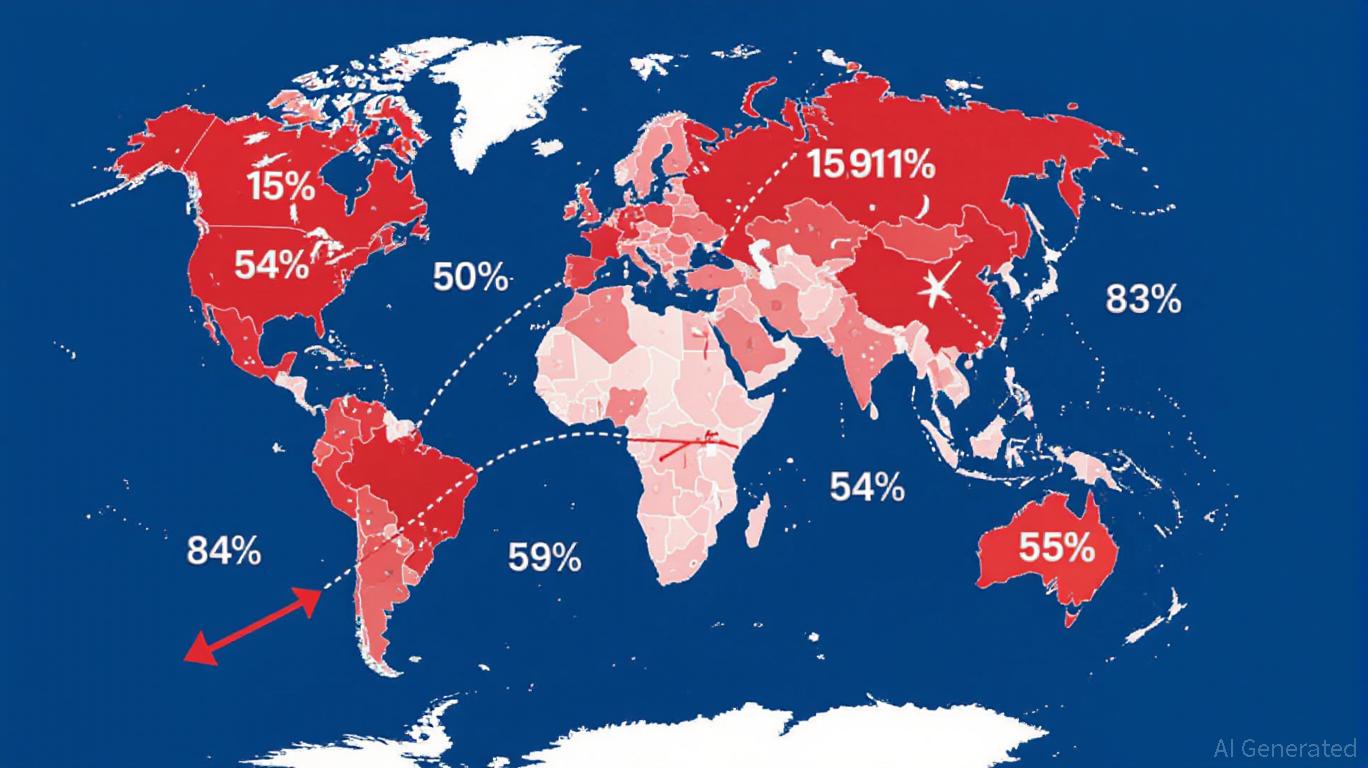

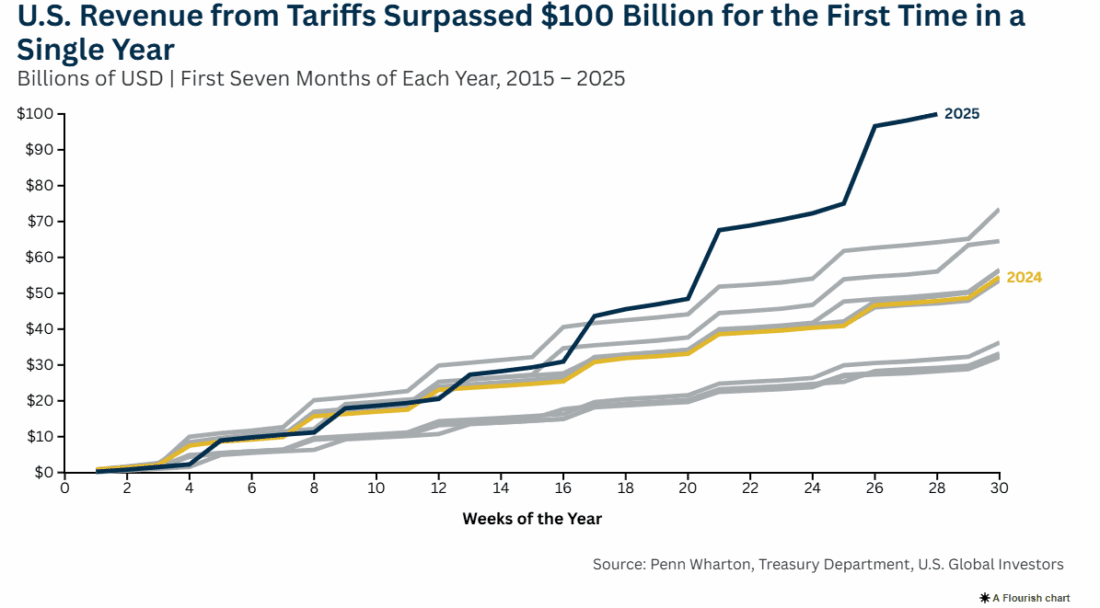

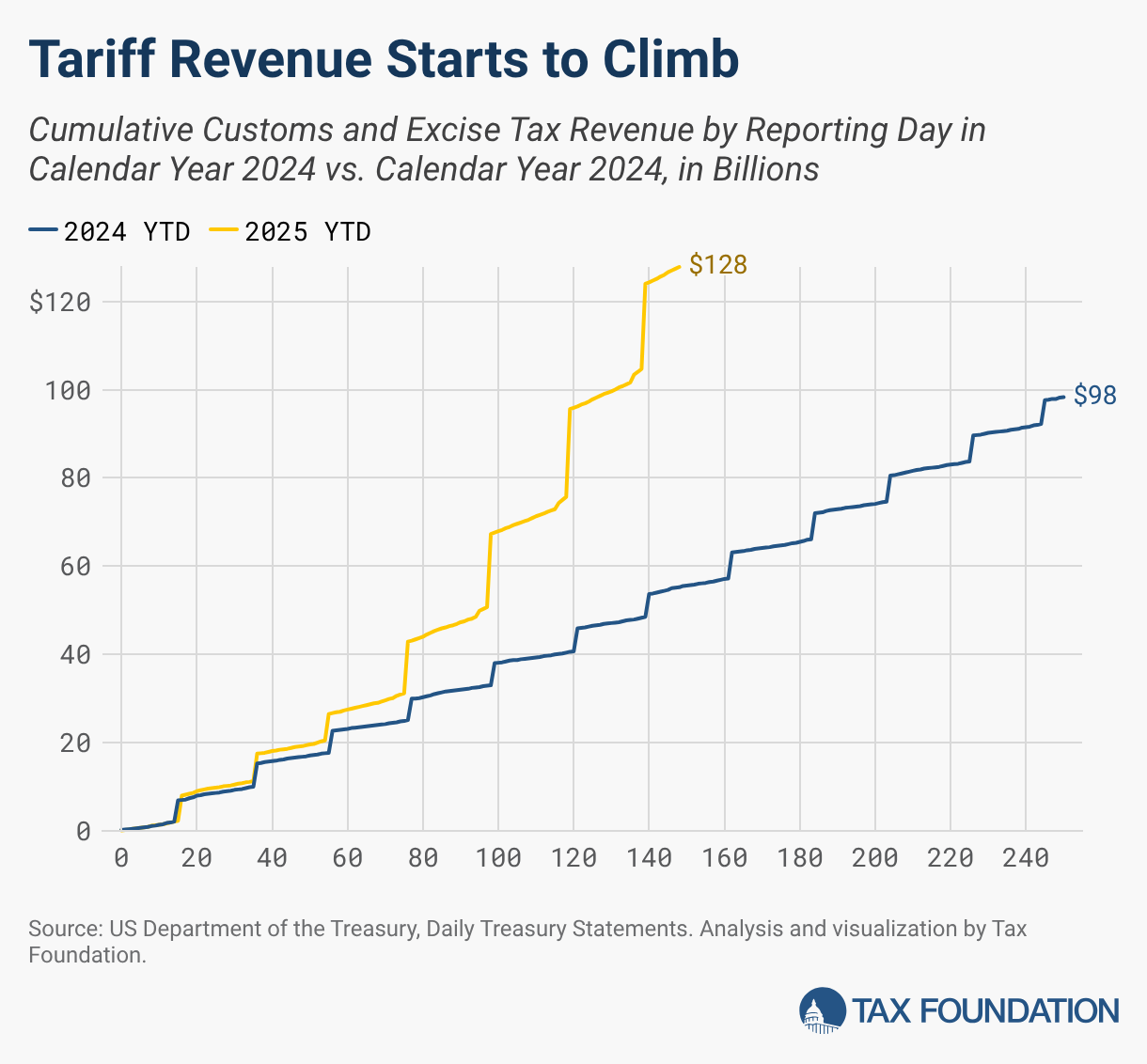

The 2018 steel and aluminum tariffs, the China trade war, and the 2025 universal tariff hikes have collectively pushed the U.S. average effective tariff rate to 22.5%—the highest since 1909.

- These policies, while aimed at reducing trade deficits and protecting manufacturing, have instead inflated input costs for downstream industries.

For instance, U.S. automakers now face 25% tariffs on imported vehicles and parts, raising consumer prices by up to 11.4%.

Similarly, the 50% tariffs on copper and aluminum have destabilized markets, with London Metal Exchange (LME) prices for copper projected to dip below $9,100/tonne in Q3 2025 as demand shifts to alternative markets.

Ask Aime:

Are 2025 tariffs set to disrupt supply chains further?

The ripple effects extend beyond the U.S.

- China's retaliatory tariffs on American agriculture and

- Brazil's 50% tariffs on U.S. imports have created a domino effect of trade retaliation.

- .P. Morgan estimates that these policies could reduce global GDP by 1% in 2025, with spillover effects doubling that impact.

- Emerging markets, particularly China and Brazil, face sharper contractions, while the U.S. could see a 0.6% permanent drag on GDP growth.

Ask Aime:

Predict how tariffs will impact U.S. auto industry?

Equity Market Volatility and Sectoral RealignmentsEquity markets have mirrored the uncertainty.

- The S&P 500, a bellwether for U.S. corporate performance, has oscillated within a narrow range of 5,200–5,800 since 2025, reflecting investor caution.

- Defensive sectors like utilities and healthcare have outperformed, trading at valuations below long-term averages, while cyclical industries such as manufacturing and commodities face headwinds.

Daily

Weekly

Monthly

Consider

, a case study in sectoral realignment.

- While the company initially benefited from U.S. protectionism by avoiding Chinese competition, its exposure to global supply chains (e.g., lithium from Latin America, batteries from South Korea) has made it vulnerable to trade disruptions.

- Its stock price, which surged during the early stages of the tariff war, has since stabilized as investors factor in long-term risks like higher component costs and regulatory scrutiny.

The automotive sector offers another lens. Domestic automakers like Ford and

have gained short-term market share by absorbing tariff costs, but their margins remain under pressure.

- Meanwhile, global automakers, particularly those in Europe and Asia, are pivoting to new markets, with Japanese firms leveraging lower tariffs under the U.S.-Japan agreement to boost exports.

Long-Term Investment Risks in a Fragmented World

The most pressing risk lies in the erosion of global economic efficiency.

- Tariffs have forced companies to rewire supply chains, increasing costs and reducing economies of scale.

- For example, U.S. pharmaceutical firms now face potential 200% tariffs on imports, which could delay drug approvals and drive up healthcare costs.

- Similarly, the 10% universal tariff on non-NAFTA partners has reduced U.S. exports by 18.1%, with Canada's economy projected to shrink by 2.1% in the long run due to retaliatory measures.

Investors must also contend with the regressive impact of tariffs on consumer spending.

- The 2.3% average price increase from 2025 tariffs has reduced real disposable income, potentially slowing GDP growth by 0.3–0.4 percentage points.

- This dynamic is particularly concerning for equity markets, as consumer-driven sectors like retail and hospitality face weaker demand.

Opportunities in a Rewired Global EconomyDespite these risks, fragmentation creates new opportunities.

- Latin America, for instance, is emerging as a beneficiary of U.S. trade realignments.

- Countries like Brazil and Mexico, with abundant raw materials and lower production costs, are attracting capital inflows.

- J.P. Morgan forecasts that Brazil's GDP could grow by 0.3–0.5% if it diversifies exports away from the U.S.

- Similarly, Vietnam's 20% tariff increase on U.S. goods has spurred investment in alternative trade routes, positioning it as a manufacturing hub for Southeast Asia.

Technology and AI sectors also present asymmetric opportunities. While near-term volatility has pressured AI equities, the structural demand for compute power remains intact.

Firms like

and

- , which supply semiconductors for AI infrastructure, continue to see robust demand as U.S. tech giants invest $315 billion in AI expansion.

- Investors who adopt a bottom-up approach, targeting companies with pricing power in the AI stack, may outperform broader indices.

Strategic Recommendations for Investors

- Diversify Beyond Traditional Assets:

With U.S. Treasuries losing their role as a safe haven, investors

should allocate to alternatives like gold, infrastructure, and

inflation-linked bonds. Gold, for instance, has historically enhanced

Sharpe ratios during periods of fiat currency instability.

- Prioritize Defensive Equities:

Sectors like utilities and healthcare offer downside protection.

Utilities, trading at 12x forward earnings, are undervalued relative to

their defensive profile.

- Hedge Against Geopolitical Risks:

Exposure to emerging markets, particularly Latin America, can offset

U.S.-centric volatility. However, investors should favor minimum

volatility strategies in these regions to mitigate trade-related shocks.

- Embrace Short-Duration Fixed Income: Given

the Fed's delayed rate cuts and elevated inflation, short-duration bonds

(3–7 years) provide a balance of yield and liquidity.

- Monitor AI and Supply Chain Trends:

Active management in AI-related equities, particularly those with

global supply chain resilience, can capture long-term growth.

Conclusion

The Trump-era tariff surge has left an indelible mark on global trade and equity markets.

While the immediate costs—higher prices, retaliatory tariffs, and GDP drag—are evident, the long-term impact hinges on how businesses and investors adapt.

In a fragmented world, success will belong to those who anticipate structural shifts, diversify portfolios beyond traditional benchmarks, and capitalize on asymmetric opportunities in sectors like AI and emerging markets.

As the global economy recalibrates, the key to long-term growth lies not in resisting fragmentation but in navigating it with foresight and agility.

========================================================================

United States Tariff Act 1930

Here's a summary of its key aspects:

- Purpose:

Intended to protect American farmers and industries from foreign

competition during the onset of the Great Depression by raising tariffs

on imported goods.

- Impact:

- Raised import duties on a wide range of agricultural and industrial goods.

- Triggered retaliatory tariffs from other nations, leading to a significant decrease in global trade.

- Widely considered by economists to have worsened the Great Depression, according to Investopedia.

- U.S. imports decreased by 66% and exports decreased by 61% between 1929 and 1933.

- The stock market reacted negatively to its passage.

- Legacy:

The Smoot-Hawley Tariff Act serves as a historical example of the

potentially negative consequences of protectionist trade policies on a

global scale